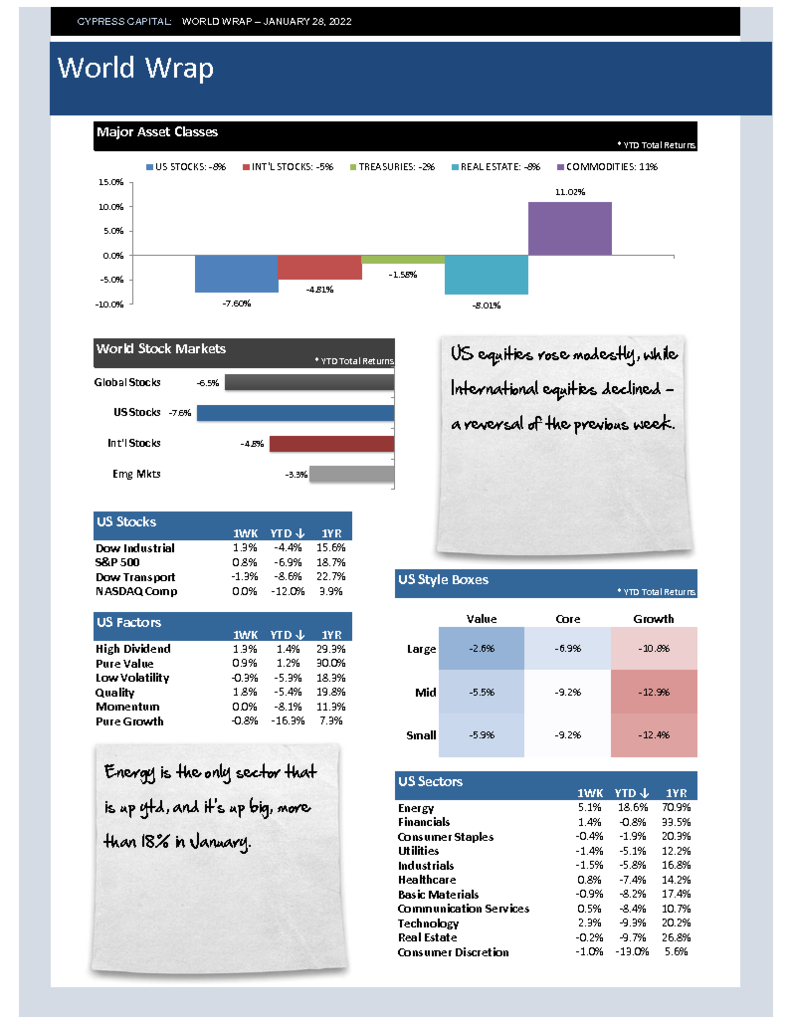

– US equities rose modestly, while International equities declined – a reversal of the previous week.

– Energy is the only sector that is up ytd, and it’s up big, more than 18% in January.

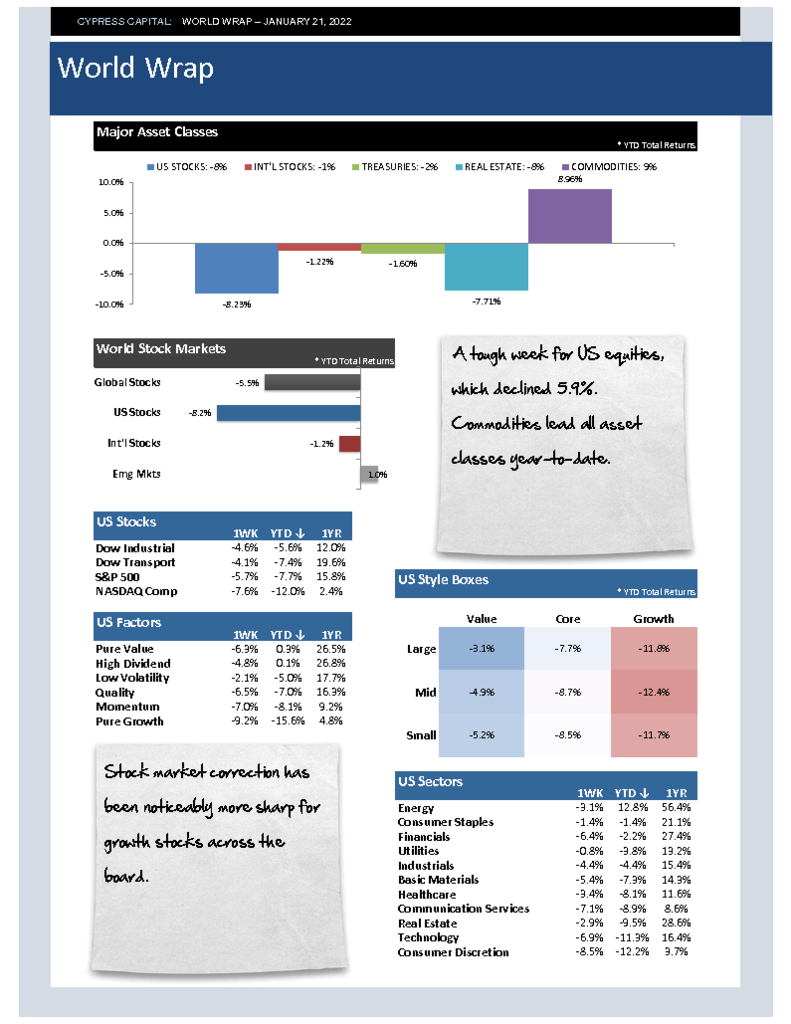

– Stock market angst finally hit Emerging markets, which turned negative on the year after falling more than 4%. China declined nearly 8%.

– Higher energy prices are largely responsible for commodity strength. Other key commodities are flat or down.